MN Paid Leave

Minnesota Paid Leave has sparked a wave of questions among small business owners – especially S-Corp owners – about who is required to participate when the program launches in 2026. One question has surfaced repeatedly in my inbox this week:

Are S-Corp owners considered covered employees under Minnesota Paid Leave, or are they exempt and allowed to opt in voluntarily?

In this post, I’ll break down:

- how the new Paid Leave program works

- how “self-employed” is defined by MN Paid Leave

- why S-Corp income reporting creates confusion

- what Minnesota Paid Leave and ADP have confirmed about owner-employees

BACKGROUND

What is MN Paid Leave?

Effective January 2026, Minnesota Paid Leave launches & provides payments and job protections for employees who take time off to care for themselves or their family.

It allows covered Minnesotan employees to take 1-12 weeks of Medical leave and 1-12 Family Leave with a maximum of 20 weeks combined if they qualify for both.

What is the cost?

Employers and employees will pay a portion of the premiums every paycheck to fund the program, and payments will cover a portion of the employee’s usual pay during the qualified leave. Employees are also ensured job protection when they return if they worked at least 90 days prior.

The premium rate will be 0.88% of employee wages, with a reduced premium rate of 0.66% for small employers. Employers can collect up to 0.44% from employees, or they can choose to cover more.

Premiums (for employers and employees) can be estimated here: Payments and time off / Minnesota Paid Leave

When do premiums get reported and paid?

Employers need to report wage details for employees and make premium payments quarterly starting in April 2026.

How do I take leave?

Applications can be submitted online or by phone. You can apply for Paid Leave up to 60 days before your leave will begin. If you can’t apply ahead of time, you can apply and take Paid Leave as soon as you know you need it.

Applications will be available starting January 1, 2026: Get ready to apply | Minnesota Paid Leave

What conditions qualify for paid leave?

Paid leave includes: medical leave, bonding leave, caring leave, safety leave, and military family leave.

Some of the qualifying events for Medical & Family leave mention the need for a “serious health condition”. This is not clearly defined at first glance, but deep within the FAQs MN provides clarification. Generally, a serious health condition prevents the employee from working at least seven days, requires inpatient admission or continuing treatment, and can include: physical or mental illness, injury, impairment, pregnancy, a chronic health condition, a permanent or long-term condition, a condition that requires multiple treatments, or an event that requires follow-up visits.

You can learn more about qualified types of leave here:

How much do employees get paid?

The weekly benefit calculation can be found here: Premium rate and contributions / Minnesota Paid Leave

SELF-EMPLOYED INDIVIDUALS

MN Paid Leave Definition

Self-employed individuals and independent contractors are not covered by Paid Leave but can opt in. If you opt in, you will pay premiums annually and will be covered under Minnesota Paid Leave for at least two years, or until you opt out. To opt in, you will need to provide documentation of your total earnings.

MN Paid Leave provides the following definition of self-employed in their FAQ:

Who is self-employed – Am I considered self-employed?

For Paid Leave, you qualify as self-employed if:

· You are an independent contractor,

· You are a sole proprietor,

· You are a single-member LLC,

· You are a general partner in a partnership,

· You are a general partner in an LLC taxed as a partnership, or

· You are otherwise in business for yourself, meaning you are not a W-2 employee. This includes freelancers and gig workers (like rideshare and delivery drivers).

Self-employment earnings are calculated on IRS Schedule SE. If you report more than $3,900 on Schedule SE, you qualify as self-employed. To learn more about who is self-employed, visit the IRS Self-Employment webpage.

(Source: Opt in to Paid Leave | Minnesota Paid Leave)

Are S-Corp Owners Covered Under Minnesota Paid Leave?

Minnesota’s new Paid Leave program has raised a surprisingly common question for small business owners:

Are S-Corp owners considered “self-employed,” or are they treated as employees who must participate in Paid Leave?

The state’s FAQ defines “self-employed” very narrowly – referring to individuals whose earnings are calculated on Schedule SE and who pay self-employment taxes.

But S-Corp owners are different. Their income is split into two categories:

- W-2 wages (reasonable compensation) – reported on Box 1 of the Form 1040

- Net S-Corp income – reported on Schedule E, not Schedule SE

This distinction matters because it implies that S-Corp owners are not considered self-employed for Paid Leave purposes, should be treated as covered employees, and must report/pay Paid Leave premiums on their W-2 wages.

Because the statute and FAQ weren’t entirely clear, I reached out directly to MN Paid Leave and an ADP Representative to confirm.

My Email to MN Paid Leave

I asked whether a single-owner S-Corp (who is an employee of their corporation and takes reasonable W-2 wages) is considered:

- self-employed and eligible for optional participation

or - an employee who must participate

I also asked whether Minnesota’s Unemployment Insurance exemption for owner-employees extends to Paid Leave. Under UI rules, corporations owned 25% or more by one person can choose not to cover owner wages unless they opt in. I wanted to know if a similar exemption would apply here.

Response From Minnesota Paid Leave

MN Paid Leave responded to the issue clearly:

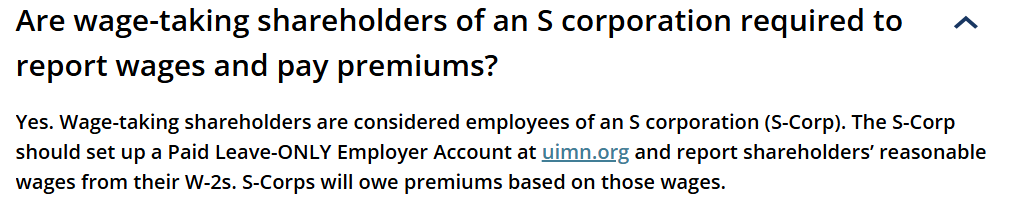

If you take W-2 wages as a shareholder, you are considered an employee. Participation in Minnesota Paid Leave is mandatory.

They stated:

- Wage-taking shareholders must set up a “Paid Leave Only” account on the MN UI website.

- They must report their wages.

- They are covered under the program like any other W-2 employee.

- This applies both to the owner and to any W-2 employees they hire.

In short:

If you take wages → you’re an employee → you are covered → you must participate.

The exemption for owner-employees that exists under Minnesota Unemployment Insurance does not apply to the Paid Leave program.

The MN Paid Leave team also noted that they’re available for questions Monday–Friday, 8:00 a.m.–4:30 p.m. CST at 651-556-7777 or 844-556-0444.

*MN emphasized that the information contained in their email is for informational purposes only and does not constitute legal or financial advice. Their email may not be construed as a determination or decision under the Paid Leave program.

However, they must have received many requests for clarification because they finally added this topic to their FAQ!

Source: https://pl.mn.gov/common-questions

ADP’s Response

My ADP representative confirmed that ADP is already preparing for this rollout and provided the same interpretation:

- Minnesota Paid Leave applies to anyone who receives W-2 wages, including single-owner S-Corps.

- If you receive W-2 wages, you do not qualify for the self-employed exemption.

- Additionally, employers must track the ESST (earned sick & safe time) accrual of 1 hour per 30 hours worked and maintain records in case of a Department of Labor audit.

- For ADP clients, required tracking features will begin rolling out in January 2026.

ADP clearly stated:

If you receive W-2 compensation, you’re a covered employee and not exempt.

Final Takeaway for S-Corp Owners

If you operate as an S-Corp and pay yourself reasonable W-2 compensation:

- You are covered under Minnesota Paid Leave

- You must register, report, and pay premiums on your wages

- You are not considered self-employed for this program

- You cannot opt out, even if you are the only employee

This may come as a surprise to many S-Corp owners who were relying on unemployment insurance exemptions, but Paid Leave is structured differently and does not offer the same carve-out.

Leave a Reply

My name is Ariana (my friends call me Ana) and I'm a CPA in Minnesota who is passionate about taxes & small businesses!

Read more about me

Meetings by Appointment

2230 Carter Ave, Suite #9

Client Portal Access Here